Assisted Living in Germany 2019

Market for care properties in transition

Germany is ageing. As a result of changing life plans, the residential market is becoming ever more differentiated.

Need for care to grow massively by 2050

Already one in four people 75 or over and more than one in three people 80 or over are care-dependent. the number of care-dependent patients covered by statutory care insurance alone who use outpatient care will increase by around 50% by 2050, while the number needing residential care will increase by 74%* over the same period.

Depending on which scenario is used**, the total number of people requiring care in Germany will rise to nearly 5 million in the next 20 years and will be close to 6 million by 2050.

With advancing age, issues such as assistance, support and care become more central to the choice of where to live and in what type of property. Continuing from last year’s detailed JLL report on “Care Homes in Germany”, the focus in this report is a short update on the care home market on the one hand, and the assisted living sector on the other.

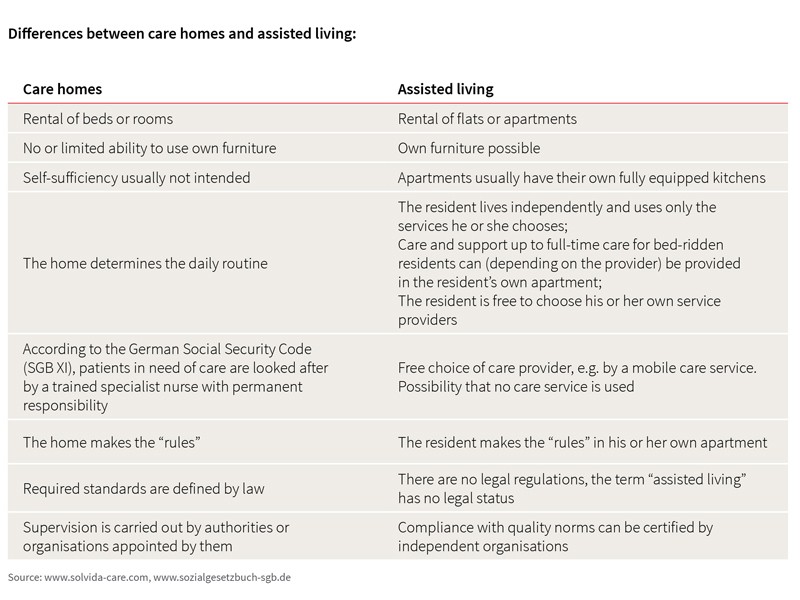

The concept of assisted living: independence with support

Living autonomously with support as required:

Assisted living facilities, which are generally designed to be barrier-free, provide communal facilities as well as apartments. Residents can also use support services and take part in leisure activities. This guarantees the private sphere and control over the living accommodation but there are possibilities to participate in social activities and make a contribution. To the extent that care is required, both relatives and professional providers can play a role.

The various concepts of this form of accommodation and care are becoming more individual and more innovative. There are around 7,000*** assisted living facilities in Germany and the number is increasing. Assisted living is now the second most common form of specialist residential property after care homes. This growth is indeed necessary since the demand often outweighs the supply in the full-time inpatient care segment.

Care requirement per care place

The map clearly shows that especially in parts of Lower Saxony and Rhineland-Palatinate, and also in Baden-Wuerttemberg and Bavaria, the number of patients in need of care outweighs the supply of full-time residential care places.

In these areas the potential demand will not be met, at least in the short-term.

There is also a massive supply shortage in the assisted living segment, so the sector can be seen as having enormous potential.

Concepts which offer a combination of assisted living and residential care can be very complementary.

Further contents of the report:

• Which care preferences do the people in Germany have?

• How can the potential future demand for care places in all cities and administrative areas be assessed?

• In which cities and counties does most of the construction activity take place?

• Which framework conditions are likely to fuel the powerful growth of assisted living?

• How is the investment demand for assisted living facilities and healthcare properties?

• Which criteria should assisted living facilities fulfil in order to qualify as a core product for investors?

* WidO press release 8th July 2019.

** Here: co-ordinated population projection by age group (variant 4) compared with care ratios by age group from 2017. Source: Federal Statistics Office.

*** PM Pflegemarkt GmbH, 2018